This was right in line with what I was expecting from a non-orthodox, “Hyman Minsky” point of view. As I have argued in numerous blogs, aggregate demand is the sum of GDP plus the change in debt. Now that our economy is utterly debt-dependent, the debt-financed asset-price bubbles have burst, and debt de-leveraging has begun in earnest, the economy will tank and unemployment will explode as debt-financed spending evaporates.

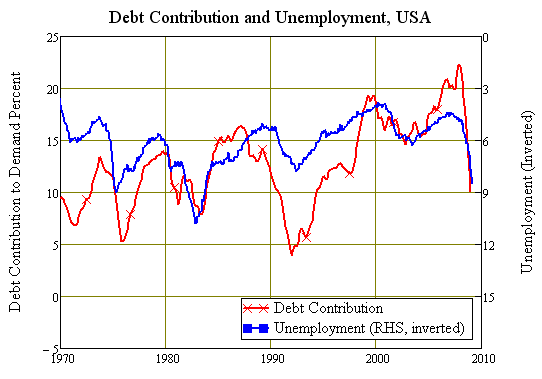

The key chart I’ve published on this a number of times is the following: it shows the correlation between the contribution the change in private debt makes to aggregate demand and the unemployment rate (the red line is the change in debt, divided by the sum of the change in debt plus GDP; the blue line is unemployment, inverted and plotted on the right hand axis).

As the economy has become more and more debt-dependent–as the ratio of Debt to GDP has risen–this correlation has gone from being trivial to explaining 95% of the level of unemployment.

For those who believe that “Australia is different”, here’s the matching chart for the USA. The only difference is one of time: they began their decline in this Depression about a year before we did. But we are rapidly catching up.

The dramatic deterioration in the economy comes as a surprise to conventional “neoclassical” economists because they exclude debt (and money) from their model of how the economy works. This failed model of the operations of a market economy is why they are incapable of explaining the economy’s behaviour today.

With the debt contribution to demand now plummeting, unemployment will rise to levels that are unprecedented in the post WWII period–and they may even rival the Great Depression.

Attempts to inflate our way out of this via either government spending or quantitative easing will also fail.

The sheer scale of private debt de-leveraging swamps the government’s pump priming, while there is so much debt relative to government created money that the latter will have to be increased by astronomical amounts–and given to those in debt, rather than to the banks–to counter the collapse in demand caused by private deleveraging.

To labour a comparison I’ve made numerous times, Rudd’s stimulus package will inject $42 billion into the economy, but a 5% reduction in debt by the private sector will remove $100 billion from it.

Even the slowdown in debt accumulation will swamp the government’s stimulus. In 2007-08, the last year of our debt bubble, private debt rose by $259 billion–adding 20% to aggregate demand. The fall of this to zero–a simple stabilisation of private debt–will remove 20% of demand from the economy. This is what is causing unemployment to explode now.

On the monetary front, Bernanke has literally doubled government-created money in the USA in a matter of months, but even so the ratio of private debt to this is close to 30 to 1. He’d need to create twenty times as much (and give it to the debtors to cancel their debts, rather than to the banks in a futile attempt to maintain their facade of solvency) before there would be any chance of a monetary stimulus working. I simply can’t see him trying it.

Even if he did (and our local RBA followed suit), and even if governments maintained the scale of fiscal stimulus they are now imparting, there would still be the reality (for the USA, the UK and Australia, and some European nations) that, courtesy of the globalisation of production, they no longer have the productive capacity to employ those who are going to be thrown into unemployment via this debt-driven collapse.

The problems caused by the neoclassical economic philosophy of the last 40 years were papered over by debt. To steal a phrase from Warren Buffett, now that debt is collapsing–and debt-finance can no longer be used to purchase cheap Asian goods–the nakedness of that philosophy will be exposed by the outgoing tide.

Australia, which has for some time deluded itself that it is different to the rest of the world, and will therefore come through this crisis relatively unscathed, may in fact be the most naked of all.

http://www.debtdeflation.com/blogs/2009/04/09/whod-a-thought-it-unemployment-leaps-05-in-a-month/

No comments:

Post a Comment